SAND SPRINGS, Okla. — Mandy Graham knew her spacious, attractive dream house on the Arkansas River was in a 100-year floodplain, but when she bought it in 2017 — with the help of a federally funded flood insurance plan — it had been just 31 years since Tulsa’s largest-ever flood.

By her math, that meant she had 69 years to go before there would be anything to worry about.

Two years later, the rains came and didn’t stop until her home was under 6 feet of water.

Local officials would later tell the hundreds of people who lost their homes that the Town and Country development in the suburbs of Tulsa never should have been built. A dried-up streambed runs smack through the middle of the subdivision — it functioned as a flood superhighway when the Arkansas crested its banks. All told, the flooding in May 2019 damaged 913 homes in the Tulsa area, destroying 335 of them, according to the Federal Emergency Management Agency.

“There's hundreds of houses over there, you know?” Graham said, referring to Town and Country. “If people actually thought it was gonna flood, would they live there?”

For decades, lawmakers and federal agencies in Washington, D.C., have resisted taking harsh action to pull federal insurance funding from especially vulnerable areas, even as climate change made a mockery of 100-year projections of the type that Graham counted on. Now, in the wake of disasters including the deadly Kentucky floods and Hurricane Ian, official Washington is openly wrestling with what to do about the hundreds of thousands of people who are living in areas that climate change is making too risky to inhabit. The fate of Graham’s home, and many thousands of others, is in the balance.

It’s a question with implications far beyond those whose homes are endangered. If large numbers of communities are rendered undesirable because of their climate, local and regional real estate markets could tank. Expensive public infrastructure like water treatment systems and roads could be abandoned or become obsolete as people relocate. Heavy taxpayer spending is likely. Yet many experts say that proactively steering people away from places climate change is making nonviable will seem a bargain compared with the costs of rebuilding in the shadow of past and future disasters, floods and droughts.

“There are places too risky for human habitation,” said Chad Berginnis, executive director for the Association of State Floodplain Managers.

But Washington is taking a cautious approach. It’s a tricky business, prodding people to leave places where they’ve lived for decades, in some cases raising families and watching relatives grow old and die. And for now, Congress is trying to use carrots rather than sticks. Lawmakers recently put “unprecedented” funding — $3.5 billion — behind efforts to move people out of harm’s way, said David Maurstad, who is FEMA’s deputy associate administrator of resilience, while federal officials have begun nudging people away from such vulnerable areas as coastal Washington state, the Mississippi River Delta in Missouri and Louisiana’s Gulf Coast.

“It shows the importance that people are now recognizing in doing something before disaster strikes,” Maurstad said in an interview. “We can't just rebuild back in the same spot, especially if we know that it's currently at risk — or that in the near future it's going to be at risk.”

The fact that official Washington is finally addressing the concept of some areas being too vulnerable to insure is noteworthy, according to people who work in a competency known as “resilience” — essentially, preparing communities to live with a changing climate.

“The interest level has never been higher,” said Rob Moore, director of the water and climate team at the environmental group Natural Resources Defense Council. “Those funding streams are now stable for the first time in their history.”

But a POLITICO investigation of federal programs showed that many of the taxpayer-backed programs are riddled with inconsistencies and bureaucracy, often impeding intended outcomes. That’s come to a head in Tulsa County, where Graham’s former Town and Country development is located.

The county secured part of a $36.4 million federal grant for disaster recovery allowing it to pay flood victims to leave their damaged homes behind, returning the land to a floodplain that will absorb the water. Such a move would save on the cost of future rebuilding and repairs, and spare county resources. Yet three years after the 2019 flood, while many have shown interest in receiving compensation in order to leave, no one in Tulsa County has collected a check.

The bureaucracy — local officials ensuring they align with federal guidelines, helping homeowners supply necessary information required for the grants — has moved slowly. Amid the delays, people who once entertained taking government cash to leave reversed course, even if it meant spending tens of thousands of dollars to hoist their homes higher.

Federal and local officials acknowledge the process can take years given the checks and balances in place — Tulsa officials said a speedy buyout takes 18 months, but more often it’s three years. FEMA data for Tulsa County backs that up: The 28 most recent buyouts in the county took 34 months on average from initiation to close. FEMA’s Maurstad said the national average is 18 to 24 months.

“These don't happen in the time frame that we would want them to happen,” he said. “We're looking at our programs to look at ways that we can reduce the complexity and help local governments in the state get through these programs.”

Given the long waits and uncertainty, however, the private company assisting Tulsa County actually advises prospective buyout winners to sell their flood-damaged homes if they find a willing buyer — perpetuating flood dangers the county and federal government are straining to solve.

“I typically advise folks: ‘Don’t wait for this program,’” said Lacie Jones, the project manager for Meshek & Associates, the local firm Tulsa County has hired to handle the grant. “We don’t want people to wait forever.”

One eligible homeowner is Mary Marris, 67. She watched her Town and Country home get flooded on TV from Atlanta, where she was visiting her son at a rehabilitation facility for a spinal cord injury. The 1986 flood had severely damaged her home already, but Marris and her husband dropped the flood insurance coverage that would have paid up to $250,000 in 2016. They’d made it 30 years — and weren’t they in the 100-year floodplain anyway?

After a second devastating blow, she was prepared to think twice about rebuilding. So when the county first contacted her about a buyout, Marris saw it as a lifeline.

“I was ready to go,” she said. “Throw in the towel.”

But years passed, and no money came. Her son, Chance, pleaded with her to keep the family home, recalling childhood memories of bounding down the backyard into the maw of the Arkansas River, where he would spend endless days fishing. He still lives nearby, but on higher ground.

Marris, like many others, decided to stay in her home. It was more than a structure, more than shelter. It meant family — even more so now. Her 64-year-old sister, Helen Dorsch, decided to buy the neighboring, flood-damaged property.

“We just wanted to take a gamble,” Dorsch said.

Managing a retreat

If the federal government wants to get people out of harm's way, it has to contend with human emotion. It throws people’s perception of danger, of risk, off-kilter. People will tolerate a lot to remain in their community, in a place of comfort. Even if it could bankrupt them. Or worse.

But as climate change makes disasters more frequent and severe, a once-taboo strategy known as “managed retreat” is getting more serious consideration in Congress and the federal government. The concept refers to relocating entire communities as climate change threatens make some places uninhabitable, whether because of rising seas or dwindling water supplies. But those involved acknowledge that the obstacles to enact such a retreat are daunting.

The families in low-lying areas of Oklahoma that were washed away in 2019 are often cited as examples of how far people will go in order to stay in their homes, even after disasters expose the risks.

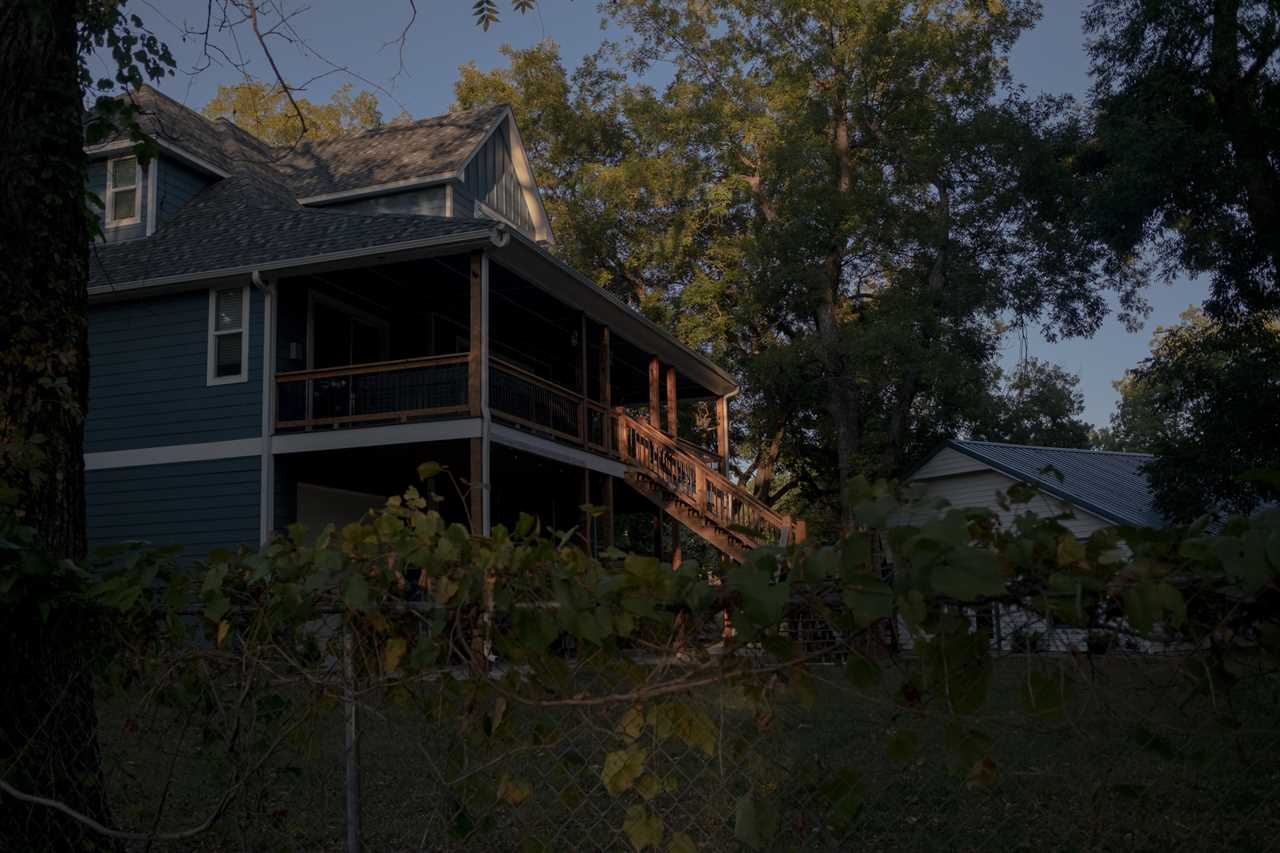

With its stilt-like structure and wooden staircase leading to a canary-yellow front door 14 feet above the ground, the royal blue home of Craig and Mary Chase looks suitable for coastal Carolina. But it sits in a secluded 18-acre pecan orchard in Collinsville, Okla., with two large garages — one for the RV, one for the boat — sitting below the deck.

The Chases lived in that RV for months after the flood with their two dogs and two cats. The county enacted provisions to keep homes safe from flooding by requiring that families like the Chases raise their homes to 9 feet above ground — a high standard. But the Chases opted to stay. They interviewed 20 builders before anyone accepted the challenge — and added an additional 5 feet in elevation, just in case.

“I feel for those people that went through the floods in Kentucky,” Craig Chase said while seated in his living room. He imagines telling them: “You have no idea what you’re about to embark upon.”

“You have to really love where you live, to fight for it,” added Mary Chase. “And fight is the key. It's a total fight.”

Leaving was never an option for Mary Chase. Her family had claims there since the Oklahoma land rush — the couple’s parcel was the last of her family’s once-vast holdings.

“His family were like, ‘Why do you ever want to move back there?’ Friends were like, ‘You're insane to build back there,’" she said before answering her own question: “It's all I've ever known.”

The few examples of U.S. managed retreat have been piecemeal — not the holistic type of retrenchment academics envision. And results have been mixed where the federal government directly intervened, such as with ongoing relocation efforts of a native community in Isle de Jean Charles, La., endangered by sea-level rise.

Still, the National Academies of Sciences, Engineering and Medicine is exploring managed retreat for the Gulf Coast in a series of workshops, hoping its inquiries will yield broad recommendations for successfully executing such a plan. The bipartisan infrastructure law also has set aside funding to help native tribes facing severe climate change threats to relocate — the Biden administration selected those tribes earlier this month.

Yet for the most part, the federal government is addressing retreat from the edges and margins. When a disaster happens, there’s stricter flood standards for rebuilding with federal dollars. Or there’s more money available to buy out flooded homes. Or there’s new permission to use funds for developing stronger building codes. Or there’s sharply increasing flood insurance premiums that could make living in some places much more costly.

“We’re in a period of time where we’re in a transition about how we think about disaster recovery,” FEMA’s Maurstad said, adding that managed retreat is “certainly a more acceptable discussion than what it was in the past.”

Managed retreat is a hard concept to swallow. On top of all the complicated dynamics of cultural attachment, communities and place, the term itself suffers from a branding issue. Who wants to admit they’re retreating, a word synonymous with defeat?

Even places like Tulsa, which have enacted policies designed to entice people to relocate, only do so after a disaster strikes.

“It was losses that got them there,” said Roy Wright, president of the Insurance Institute for Business and Home Safety, who was previously chief executive of FEMA’s National Flood Insurance Program. “You’re only going to be dealing with this relocation reality where disasters are happening, where losses are happening. Nobody is going to have the foresight.”

Gary McCormick, Tulsa’s senior special projects engineer, said most people remain resistant to a buyout unless they actually experience a flood.

Yet the city still notifies homeowners of their flood risks and offers buyouts. New federal funding will help them do more. McCormick walks homeowners through the flood maps and the risks, spelling out the costs for damage. Some take the city up on the offer. Most don’t.

“They're still just resistant,” McCormick said. “That's frustrating. Just being one who wants to help people, keep them out of harm's way, keep them from flooding, and experiencing all that goes with that.

“The optimum solution is just to move people out of harm's way,” he added.

No clear signal

But there’s a major divide between experts like McCormick and elected leaders. In Florida, elected officials are pledging to rebuild. Many want to restore communities right in Ian’s footprint. It’s only natural: People have to live somewhere, and these somewheres were people’s homes.

Given how many people elected to stay put in Sand Springs, many people will also likely choose to return to Florida’s Gulf Coast — even if the federal government is growing more assertive about the perils people face by remaining in place.

“The signal from the federal government is that we’re taking resilience seriously,” said Natalie Enclade, executive director at BuildStrong Coalition.

But the view on the ground from places like Tulsa reveals major faults in the execution, which Enclade said boils down to: “Throw money at it, hold our nose and close our eyes — and hope it gets better.”

The federal grant that Joe Kralicek is using for the buyouts in Graham’s old Town and Country neighborhood is over-subscribed — 180 people in the county have signed up, but Kralicek only has funding for 60.

It’s a Department of Housing and Urban Development grant. That means it comes with income restrictions: At least 70 percent of the state’s $36.4 million HUD Community Development Block Grant must benefit low- and middle-income people. Many who are interested, whose homes are decimated, are ineligible for income reasons. The HUD program is so complicated that most governments fail to spend the money it offers.

So Kralicek, who is the emergency manager for Tulsa and Tulsa County, is looking at another program through FEMA. But the county is struggling to come up with the money to cover the 25 percent federal match FEMA requires. Instead, Kralicek is using some of the HUD grant as the match for the FEMA award.

That means people like Barb Jackson are left in limbo as local officials juggle the complicated buyout process.

The 79-year-old Jackson officially retired from teaching in Tulsa Public Schools in 2016 after earning enough to redo the kitchen and pay for other renovations to the home. But the floods ravaged it — and contaminated the land, fouling the air.

The county said she would have to elevate the home to prevent future flooding. Jackson moved out instead. Living on a fixed income, she’s making mortgage payments for the first time in her life. She said she worries nonstop about money and grieves the loss of her home. The result has been anxiety, depression and three hospital visits since the flood.

The buyout would bring peace of mind and stability, even if it won’t bring Jackson’s home back. “It gave me hope,” she said. But she’s still waiting.

“I'm devastated. And even though people say get over it, you can't get over it. So it's like losing a family member,” she said. “Everything was paid off. And at my age, starting over again, I feel like I'm in a pit and can't climb my way out.”

Making people pay

One way to push people to make rational decisions is to force them to pay more if they don’t.

In October 2021, FEMA rolled out its long-awaited revamp to the federal flood insurance program, known as Risk Rating 2.0. The effort aims to align insurance premium pricing with the actual flood risk homes face. FEMA hopes doing so will limit losses to the chronically indebted, taxpayer-funded federal flood insurance program and also signal to would-be homeowners that some places face significant danger.

“There is no greater risk-communication tool than a pricing signal. When we distort the price, we distort their understanding of risk,” said Wright, the former FEMA flood insurance chief.

FEMA is also weighing new regulations that would expand the federal floodplain, which could include increasing minimum requirements for elevating homes to reduce flood risk. Those rules could be a “game changer” by requiring stricter building standards to reduce flood risk for hundreds of local governments, said Berginnis of the Association of State Flood Plain Managers. The rules have remained largely unchanged since 1976, before the broader public even heard of global warming.

The White House also has convened an interagency effort to update building codes. The Biden administration hopes it can entice local and state governments to adopt the types of measures that kept many Ian-whacked Florida buildings upright.

Meanwhile, Reps. Sean Casten (D-Ill.) and Earl Blumenauer (D-Ore.) have sponsored legislation that would more quickly purchase severe repetitive loss properties to lessen the taxpayer burden on bailing out those homeowners. The bipartisan infrastructure law also gave FEMA authority to start a new pilot program in flood-ravaged states that connects flood victims more quickly with federal dollars.

But such modest steps aren’t nearly enough to overcome the many pitfalls.

While the federal government encourages new building codes, they’re merely voluntary. Roughly 30 percent of construction in the U.S. today occurs in places with outdated building codes, said Gabriel Maser, vice president of government relations with the International Code Council, which develops model codes. Only one federal agency — FEMA — includes minimum standards for building codes, though a federal government-wide standard “is certainly something we’ve raised” with the administration, Maser said.

When Oklahoma accepted federal funds for the buyout program, it rejected ICC’s recommendation to require local governments that would receive those dollars to update their codes, in part because the codes were seen as too costly.

Risk Rating 2.0 also brought unintended consequences. The new pricing worked as intended: Premiums rose for homes with more flood risk. But more than 300,000 people responded by dropping coverage. Many of those people were in Florida. The number of Sunshine State policies fell by 3 percent — roughly 48,000 homes — between the October 2021 rollout and Ian’s landfall on Sept. 28, according to First Street Foundation, a group that analyzes flood risk.

The federal government also has not set common language, targets or standards for how to assess future climate risk with the hundreds of billions of dollars they’re shoveling to states through the infrastructure law.

That’s led some to fear that infrastructure will fail in future climate conditions — that the government is doubling down on places people should be leaving.

“We are in the position of doing buyouts now in part because of development choices that we all made in the past,” said Anna Weber, a policy analyst at NRDC who works on floods. “We don’t want to be making development choices today that put us in the same position 30 years from now.”

Lessons from the past

Ironically, a lesson from Tulsa’s past could serve as a model for flood-fighting in America.

The city’s population exploded almost overnight in the 1950s and 1960s as it annexed neighboring communities, moving into the Mingo and Joe creek watersheds. By the 1980s, flooding occurred nearly every year. Then the great 1986 flood forever changed the flat, mid-sized city carved by creeks and fueled by oil and gas money.

The wreckage from that catastrophe was so severe that citizens taxed themselves with a stormwater fee to pay for new drainage infrastructure — and to buy out, demolish and relocate flood-prone homes.

All told, Tulsa has purchased more than 1,000 flooded properties since the 1970s. Its 2019 hazard mitigation plan targeted 88 additional properties — buildings that have made more than one $10,000 claim through the federal flood insurance program. Those efforts and other investments this year made Tulsa the second community in the country — the other is Roseville, Calif., near Sacramento — with FEMA’s top rating for reducing flood risk, cutting its residents’ insurance premiums by 45 percent.

“There's no way we could have accomplished as much as we did in that time without the federal partnership,” Tulsa Mayor G.T. Bynum said in an interview. Tulsa has since applied for more federal funding for flood prevention, including a $20 million grant from FEMA’s Building Resilient Infrastructure and Communities program, which received $2.3 billion in the bipartisan infrastructure law — a nearly five-fold increase from 2019 levels.

Kralicek grew up in one of those flood-prone homes. The entire Tulsa neighborhood where that home once rested is now a park, a natural sponge.

“A lot of these buyouts are really local government going, ‘You know what? We messed up by letting people build houses in that neighborhood. That should have never happened,’” Kralicek said.

Yet people keep moving to these places, in part because the government has done a poor job publicizing the risks.

Some of Graham’s neighbors in the Town and Country development weren’t legally required to buy flood insurance because they were in the less risky 500-year zone. But FEMA’s flood maps are outdated, with thousands more homes facing flooding than FEMA’s maps acknowledge. When the 2019 flood hit, the bank repossessed Graham’s neighbor’s uninsured home.

“I could never live in that neighborhood ever again. Even just driving down there gives me so much anxiety, even just to check on the house and stuff like that,” said Graham, who is still waiting on her buyout from the federal government. “I don't think that that neighborhood ever should have been built. You're building homes just for them to be destroyed.”

Kralicek partly blames the destruction on developers who fight against tougher building codes. He cites a statistic that has become dogma to resilience experts: Every dollar spent on bolstering buildings and infrastructure against disasters saves $7 in damages and recovery costs.

But that doesn’t mean every community heeds the advice. Local governments depend on property tax revenue, meaning there’s an incentive for growing the tax base. Major organizations like the Farm Bureau resisted state legislation that would have funded flood mitigation projects through a new fee on county property owners, saying it would burden farmers.

Kralicek, though, sees flood buyouts as part of an economic development plan. Disasters are costly. Avoiding damage frees up funds for other purposes.

“Human beings are terrible at assessing risk,” Kralicek said. “We're awful at it. Which is why things like casinos do so well.”

Recent federal policy changes might help to limit those losses. But until there’s a wholesale rethink of how — and where — cities, towns and counties develop, there will be more hardship.

“The piper is gonna come call, and at some point you got to pay,” Kralicek added. “And you just got to figure out who's paying.”

----------------------------------------

By: Zack Colman

Title: Dream homes and disasters: Is the government ready to confront climate risk?

Sourced From: www.politico.com/news/magazine/2022/11/25/fema-climate-risk-homes-00065305

Published Date: Fri, 25 Nov 2022 07:00:00 EST